What does level funded mean in health insurance?

A level funded health insurance plan combines elements of both self-funded and fully insured plans, designed to offer businesses a predictable, cost-effective way to manage health benefits. Here’s a quick look:

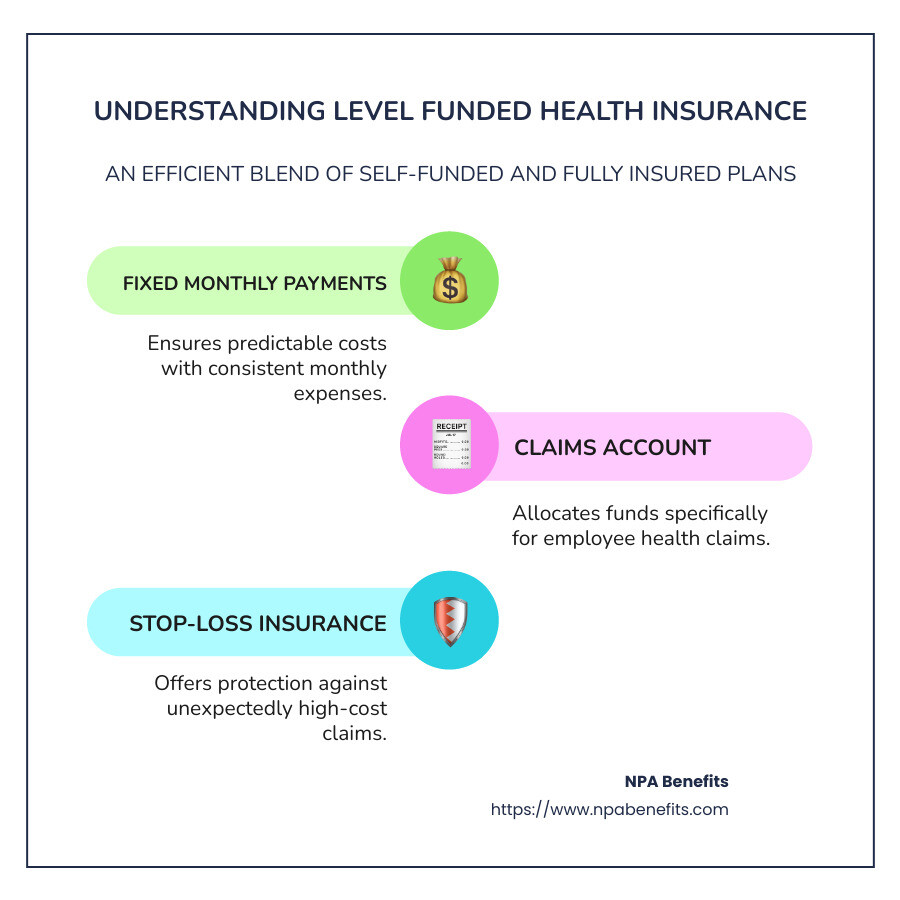

- Fixed Monthly Payments: Pay a consistent, manageable amount each month.

- Claims Account: Set money aside specifically for employee claims.

- Stop-Loss Insurance: Protect against unexpected, high-cost claims.

Understanding and navigating health insurance options can seem daunting, especially for small and medium-sized businesses. Level-funded plans simplify this task, merging cost control with flexible features. When rising premium costs can squeeze budgets, level funded plans offer standout advantages. They empower businesses to provide quality health benefits without sacrificing financial health.

I’m Les Perlson, with a rich history in health insurance, drawing from experiences in employee benefits design and health insurance solutions. My expertise centers around simplifying what does level funded mean in health insurance to improve small businesses’ benefit strategies. Stay tuned as we dive deeper into this innovative insurance approach.

Quick look at what does level funded mean in health insurance:

– fully insured health plan

– self insured plan

– aso health insurance

What Does Level Funded Mean in Health Insurance?

Level funded health insurance is a game-changer for businesses seeking balance between cost control and employee benefits. It’s like having a safety net that ensures predictability in your health insurance costs.

Predictability

One of the biggest perks of a level funded health plan is its predictability. Businesses pay a fixed monthly payment, which means no surprise costs. Imagine knowing exactly how much you’re going to spend on health insurance every month—it’s a relief!

Fixed Monthly Payments

Every month, employers make a consistent payment. This payment covers employee health claims, administrative fees, and stop-loss insurance. It’s like having a budget that doesn’t change, helping businesses plan their finances better.

Stop-Loss Insurance

Stop-loss insurance is your financial safety net. It kicks in when claims exceed a certain threshold, covering those unexpected, high-cost claims. This means businesses are protected from the financial impact of major health claims.

How It Works

- Monthly Premiums: Pay a set amount each month.

- Claims Fund: A portion of the payment is reserved for health claims.

- Stop-Loss Coverage: Protects against excessive claims costs.

Level funded plans provide a solid structure for managing health benefits, offering a predictable and stable approach to healthcare costs. They are especially appealing for small to mid-sized businesses looking to maintain control over their financial commitments while still offering robust employee benefits.

Next, we’ll explore how these plans work in detail, including the role of claims accounts and administrative fees. Stay with us!

How Level Funded Plans Work

Level funded health plans offer a unique way to manage employee health benefits. Let’s explore the nuts and bolts of how these plans function, focusing on claims accounts, administrative fees, and the potential for a surplus refund.

Claims Account

A level funded plan sets aside a portion of your monthly payment into a claims account. This account is used to pay for employee health claims throughout the year. Think of it like a savings jar specifically for healthcare expenses. If claims are lower than expected, this account can end up with a surplus at the end of the year.

Administrative Fees

Running a health plan involves more than just paying claims. There are also administrative fees. These fees cover the services provided by third-party administrators, like processing claims, onboarding participants, and offering customer service. These costs are part of your fixed monthly payment, making it easy to budget for them.

Surplus Refund

Here’s a potential bonus: if your employees’ health claims don’t use up all the funds in the claims account by the end of the year, you might get a surplus refund. This means some of the money you paid could come back to you. It’s like getting a rebate for keeping your team healthy!

Putting It All Together

To understand how these components fit together, consider this breakdown:

- Monthly Payment: Covers claims, administrative fees, and stop-loss insurance.

- Claims Account: Funds are used for employees’ medical claims.

- Administrative Fees: Pay for plan management services.

- Surplus Refund: Potential refund if claims are lower than expected.

Level funded plans offer a structured way to manage healthcare costs while providing the possibility of financial rewards for maintaining a healthy workforce. Next, we’ll compare level funded plans with other types of insurance models to help you find the best fit for your business.

Benefits of Level Funded Health Insurance

One of the biggest perks of level funded health insurance is the potential for cost savings. Unlike traditional fully insured plans, any unused funds in the claims account can be returned to the employer as a surplus refund. This means if your team’s medical expenses are lower than anticipated, you might see some money back at the end of the year. A case study mentioned in the research showed a biotech company saving nearly $400,000 over five years by switching to a self-funded model, which is similar to level funded plans. This is a big deal for companies looking to stretch their budgets further.

Flexibility

Another standout advantage is the flexibility these plans offer. Employers can tailor the plan to fit the specific needs of their workforce. This includes customizing aspects like deductibles and copayments. This flexibility allows businesses to design a plan that aligns with their budget and employee needs. It’s like having a health plan that fits your company perfectly, rather than trying to fit into a one-size-fits-all model. This customization can lead to higher employee satisfaction, as they feel their needs are being directly addressed.

Transparency

Level funded plans also bring a high level of transparency. Employers receive regular reports detailing how funds are being used, allowing them to see exactly where their money is going. This insight helps businesses make informed decisions about their health plans and encourages smarter spending. With this transparency, companies can better understand their healthcare expenses and adjust their plans to maximize benefits for both the employer and employees. This clear view into healthcare spending can be a game-changer for businesses trying to steer the complex world of employee benefits.

Next, let’s dive into how level funded plans stack up against fully insured and self-insured plans, focusing on financial risk, plan design, and employer control.

Comparing Level Funded, Fully Insured, and Self-Insured Plans

When it comes to choosing the right health insurance model, businesses often weigh the pros and cons of level funded, fully insured, and self-insured plans. Let’s break down these options by looking at three key factors: financial risk, plan design, and employer control.

Financial Risk

Level Funded Plans offer a balanced approach to financial risk. Employers pay a fixed monthly amount that covers estimated claims, administrative fees, and stop-loss insurance. This setup provides predictable costs and a safety net for high claims. If claims are lower than expected, employers may receive a surplus refund.

On the other hand, Fully Insured Plans transfer all financial risk to the insurance company. Employers pay a fixed premium, and the insurer handles all claims. This means less financial risk for the employer, but also no chance to benefit from surplus funds if claims are low.

Self-Insured Plans involve the highest financial risk for employers. They pay for claims out of pocket as they arise, which can lead to significant savings if claims are low. However, without stop-loss insurance, employers could face devastating costs from unexpected high claims.

Plan Design

Level Funded Plans provide flexibility in designing the plan. Employers can customize coverage levels, deductibles, and other features to meet their workforce’s needs. This customization is a big plus for companies wanting a custom approach.

In contrast, Fully Insured Plans offer limited flexibility. Insurance carriers typically dictate the plan design, leaving employers with few options to customize. This can be restrictive for businesses with unique needs.

Self-Insured Plans offer the most control over plan design. Employers can decide on every aspect of the plan, from coverage options to cost-sharing arrangements. This allows for a completely bespoke health plan, but it also requires more administrative effort.

Employer Control

With Level Funded Plans, employers have a moderate level of control. They can influence plan design and gain insights through detailed claims data, but they still rely on third-party administrators for administration.

Fully Insured Plans place the least control in the hands of employers. The insurer manages all aspects, from claims processing to compliance, which can be beneficial for companies that prefer a hands-off approach.

Self-Insured Plans give employers the most control over their health benefits. They manage claims and compliance directly, which allows for greater oversight but also requires more resources and expertise.

Up next, we’ll tackle some frequently asked questions about level funded health insurance, such as the differences between fully insured and level funded plans, and the potential drawbacks of choosing a level funded plan.

Frequently Asked Questions about Level Funded Health Insurance

What’s the difference between fully insured and level funded?

When comparing fully insured and level funded health plans, the main difference lies in financial risk and premium payments.

In a fully insured plan, employers pay a fixed premium to an insurance company. The insurer assumes all financial risk and manages the plan. This means predictable costs for the employer, but also no opportunity to benefit from surplus funds if claims are low.

In contrast, a level funded plan combines elements of fully insured and self-funded plans. Employers pay a fixed monthly amount that covers estimated claims, administrative fees, and stop-loss insurance. This setup provides predictable costs and a safety net for high claims. If claims are lower than expected, employers may receive a surplus refund, offering potential savings.

What are the cons of a level funded health plan?

While level funded plans offer many advantages, there are some potential costs and challenges to consider:

-

Learning Curve: Transitioning to a level funded plan may require a learning curve for employers. Understanding the intricacies of stop-loss insurance and claims accounts can be complex.

-

Potential Costs: Although level funded plans aim to control costs, there is a possibility of claims exceeding stop-loss coverage in higher cost years. This could lead to higher renewal rates.

-

Administrative Resources: Managing a level funded plan may require more resources for plan administration and compliance with regulations like ERISA.

How does stop-loss insurance work in level funded plans?

Stop-loss insurance is a crucial component of level funded plans, acting as a risk protection mechanism.

In a level funded plan, employers pay into a claims account to cover employee health claims. However, if claims exceed a certain threshold—which can be anywhere from $10,000 to $100,000 per employee—the stop-loss insurance kicks in. This insurance covers the excess costs, protecting employers from unexpected high claims that could otherwise be financially devastating.

By having stop-loss insurance, employers can enjoy the benefits of a level funded plan with the peace of mind that they are shielded from catastrophic claims.

Now that we’ve addressed these common questions, let’s dig into the conclusion of our guide, where we’ll explore how NPA Benefits can help you steer flexible and cost-saving health insurance options.

Conclusion

Navigating health insurance can be daunting, but with NPA Benefits, you have a partner dedicated to making it simpler and more cost-effective. Our focus is on providing flexible health insurance solutions that not only meet your current needs but also adapt as those needs change.

Level funded health insurance is a standout option for businesses seeking to balance cost control with comprehensive coverage. This approach offers predictable costs through fixed monthly payments while providing the potential for cost savings if claims are lower than expected. It’s a win-win scenario that gives you the financial predictability of a fully insured plan with the added flexibility and potential refunds of a self-funded model.

By choosing NPA Benefits, you gain access to a team that understands the intricacies of health insurance and is committed to delivering plans that offer both flexibility and savings. We prioritize putting control back in your hands, allowing you to customize your plan to fit your unique needs.

Ready to explore how level funded health insurance can benefit your business? Visit our health insurance benefits page to learn more and let us help you find the right solution for your team. Together, we can ensure that your employees’ health needs are met while keeping your costs manageable.