Understanding Your Health Insurance Funding Options

When it comes to fully insured vs self-insured vs level-funded health plans, employers need a clear understanding of the key differences to make the right choice for their business. Here’s a quick comparison:

| Plan Type | Risk Bearer | Cost Structure | Potential Savings | Best For |

|---|---|---|---|---|

| Fully Insured | Insurance carrier | Fixed monthly premiums | None (no refunds) | Small businesses seeking predictability |

| Self-Insured | Employer | Pay-as-you-go claims | 10-15% if claims are low | Larger companies with stable cash flow |

| Level-Funded | Shared | Fixed monthly payments | Potential refunds at year-end | Small-to-mid sized companies wanting balance |

Navigating the health insurance marketplace can be a daunting task for business owners. With healthcare costs projected to increase by 7% in 2025, more employers are exploring alternatives to traditional fully insured plans. Understanding the differences between fully insured vs self-insured vs level-funded plans is crucial for managing your company’s financial health while providing quality benefits to attract and retain employees.

Each funding model offers a different approach to balancing cost predictability, financial risk, and plan customization. The right choice depends on your company’s size, risk tolerance, and cash flow stability.

“How you pay for a plan is not as important as what you are paying for.”

This common perspective misses an important truth: your funding method significantly impacts both your costs and the quality of benefits you can offer. The right funding strategy can potentially save your business 10-15% on healthcare costs while providing more custom coverage for your employees.

I’m Les Perlson, a partner with over 40 years of experience in the health insurance industry specializing in employee benefits design and helping businesses steer the complexities of fully insured vs self-insured vs level-funded health plans. My expertise has helped countless companies find the optimal balance between cost control and comprehensive coverage for their unique needs.

Fully insured vs self-insured vs level-funded word list:

– level funding vs self-funding

– self funded insurance meaning health insurance

– self funded vs level funded

Understanding Health Plan Funding Options

When it comes to providing health insurance for your employees, understanding the different funding structures is crucial. Think of it like choosing how to pay for your company’s healthcare highway: you can pay regular tolls (fully insured), build your own road (self-insured), or enter a partnership with rebate potential if traffic is light (level-funded). Let’s explore these three approaches to help you make the best choice for your organization.

What Is a Fully Insured Health Plan?

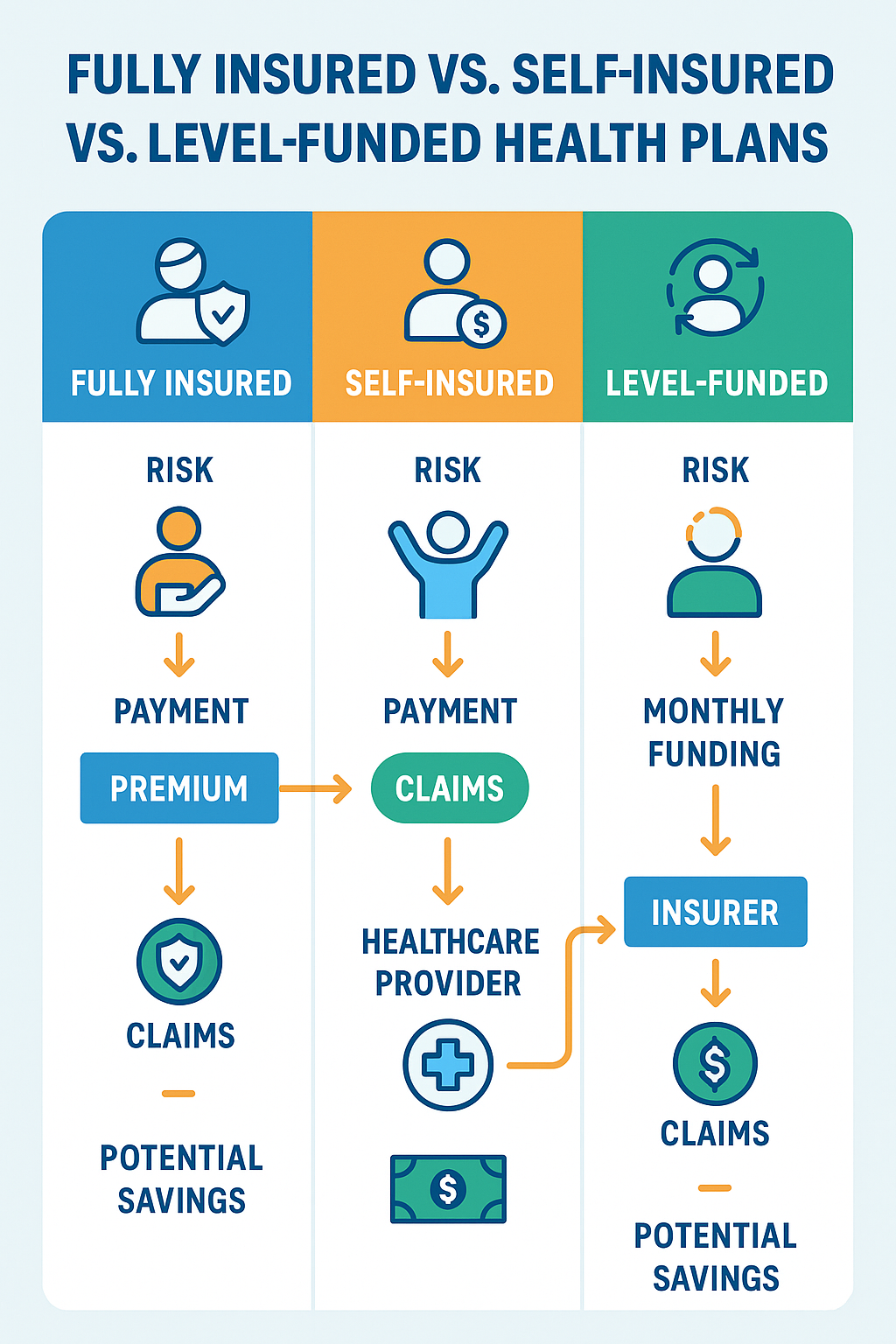

A fully insured health plan is the traditional approach most employers are familiar with. Under this model, your company pays fixed monthly premiums to an insurance carrier who then takes on all the financial risk for your employees’ healthcare claims.

As one small retail business executive told us, “With our fully insured plan, I know exactly what we’ll pay each month. It’s like having a fixed mortgage instead of a variable rate – I can budget for it precisely.”

With a fully insured plan, your premiums remain stable throughout your contract period (typically one year), changing only if your employee enrollment numbers shift. The insurance carrier handles all the claims processing, provider networks, and compliance requirements. At renewal time, the carrier reviews your group’s claims history and may adjust your rates accordingly.

Recent data shows small businesses with fully insured plans have seen premium increases averaging 5% from 2023 to 2025, with family premiums rising by 18% over the past five years. It’s like a community swimming pool – everyone contributes to maintenance regardless of how often they swim.

For more detailed information about fully insured plans, check out this helpful resource on fully insured vs self-funded health plans.

What Is a Self-Insured Health Plan?

With a self-insured (or self-funded) health plan, your company assumes the financial risk for providing health benefits. Instead of paying premiums to an insurance carrier, you pay for actual healthcare claims out-of-pocket as they occur.

According to the Kaiser Family Foundation, 67% of covered workers are enrolled in self-funded health plans in 2025. However, there’s a significant size disparity: 85% of large firms choose this option compared to only 21% of small firms.

In this model, you typically work with a Third-Party Administrator (TPA) who processes claims and handles administrative tasks while you set aside funds to pay employee healthcare claims directly. Your monthly costs will vary based on actual healthcare utilization, which provides both opportunity and challenge.

“Switching to self-funding saved us nearly $800,000 last year,” shared the CFO of a manufacturing company with 500 employees. “Yes, our monthly expenses fluctuate, but the overall savings and control over plan design make it worthwhile for a company our size.”

Most self-insured employers purchase stop-loss insurance to protect against catastrophic claims. This coverage kicks in when claims exceed a predetermined threshold, providing important financial protection while still allowing for the benefits of self-funding.

For more information about self-insured plans and recent trends, visit the Kaiser Family Foundation’s report on plan funding.

What Is a Level-Funded Health Plan?

A level-funded health plan offers the best of both worlds – combining elements of fully insured and self-insured models. This increasingly popular option gives you the predictable monthly payments of a fully insured plan with the potential cost savings and customization benefits of a self-funded plan.

Level-funded plans have seen remarkable growth, with 42% of small firms offering them in 2025, compared to just 7% in 2019.

With a level-funded plan, your company pays a fixed monthly amount to a TPA or insurance carrier. This payment typically covers administrative fees, stop-loss insurance premiums, and funds for anticipated claims. The magic happens at year-end: if actual claims are lower than expected, you may receive a refund. If claims exceed expectations, your stop-loss insurance covers the difference.

One small business owner described level-funded plans as “self-funding with training wheels,” telling us, “We weren’t ready to take on the full risk of self-funding, but we wanted more control and potential savings than a fully insured plan offered. Level-funding has been the perfect middle ground.”

These plans are particularly appealing to small and mid-sized businesses with relatively healthy employee populations. They offer the stability of predictable monthly costs while providing the opportunity to benefit financially from lower-than-expected claims.

To learn more about how level-funded plans compare to self-funded options, check out our detailed comparison on Level Funding vs Self Funding.

Understanding the key differences between fully insured vs self-insured vs level-funded plans is the first step in making the right choice for your business. Each model offers distinct advantages and challenges that can significantly impact both your bottom line and the quality of benefits you can provide to your employees.

Fully Insured vs Self-Insured vs Level-Funded: Key Differences

When comparing fully insured vs self-insured vs level-funded health plans, several critical factors come into play that can significantly impact your company’s finances and the quality of benefits you provide. These differences aren’t just academic—they directly affect your bottom line, your employees’ satisfaction, and your ability to attract top talent in a competitive marketplace.

Fully Insured vs Self-Insured vs Level-Funded: Cost Structures Explained

The way you pay for health coverage varies dramatically between these three models, and understanding these differences can help you make the right choice for your business.

With fully insured plans, you’re essentially paying for certainty. Your monthly premiums are fixed, making budgeting straightforward—you know exactly what you’ll pay each month regardless of how many claims your employees file. These premiums include expected claims costs, administrative fees, the carrier’s profit margin, risk charges, and applicable taxes. The downside? Even if your employees barely use their insurance, you won’t see a penny back. It’s like paying the same car insurance premium whether you drive 5 miles or 5,000 miles a month.

Self-insured plans operate more like a pay-as-you-go system. Your monthly costs fluctuate based on actual claims filed by your employees. You’ll pay administrative fees to a Third-Party Administrator (TPA), stop-loss insurance premiums, and the actual healthcare claims as they occur. This approach can lead to significant savings—typically 10-15%—when claims are lower than expected. Plus, you’re exempt from certain state premium taxes, putting more money back in your pocket. The challenge? You need robust cash flow to handle those inevitable months when claims spike.

Level-funded plans offer a middle ground that many businesses find appealing. You make fixed monthly payments (similar to fully insured plans), but there’s a potential bonus at the end of the year: if claims are lower than projected, you may receive a partial refund. These monthly payments cover administrative fees, stop-loss insurance premiums, and estimated claims costs based on your group’s demographics. According to industry data, companies pay about 19% less on average with level-funded plans compared to fully insured plans.

As one HR director told us after switching to a level-funded plan: “We get the predictability we need for budgeting, plus the excitement of a potential year-end bonus. Last year’s $42,000 refund funded our entire wellness program—a win-win for everyone.”

Fully Insured vs Self-Insured vs Level-Funded: Financial Risk and Stop-Loss Insurance

Who bears the financial risk for healthcare claims is perhaps the most fundamental difference between these plan types.

With fully insured plans, the insurance carrier assumes 100% of the financial risk. If an employee needs an expensive medical procedure, that’s the carrier’s problem, not yours. Your premiums won’t change during your contract period (typically 12 months), regardless of how many claims your employees file. The carrier pools risk across all their groups, which means you’re essentially sharing costs with other companies (this is called community rating).

In self-insured plans, your company steps into the insurer’s shoes and assumes the primary financial risk. This doesn’t mean you’re completely exposed, though. Stop-loss insurance serves as your safety net, protecting against catastrophic claims. There are two types: individual (specific) stop-loss caps your liability for any single claim, while aggregate stop-loss limits your total annual claims exposure. Without this protection, a single major health event could devastate your finances.

Level-funded plans offer a balanced approach where risk is shared between your company and the insurance carrier. Built-in stop-loss coverage protects you against both high individual claims and unexpectedly high overall claim volume. As one insurance expert explained: “The stop-loss policy includes mechanisms to cover short-term deficits when actual claims exceed the estimated claims upon which monthly contributions were based.”

The value of stop-loss insurance can’t be overstated. One of our clients shared a sobering story: “When our employee needed an $800,000 liver transplant, our stop-loss insurance kicked in after $50,000. Without that protection, we might have faced bankruptcy instead of celebrating our employee’s recovery.”

Plan Customization and Flexibility

The ability to tailor your health plan to your workforce’s specific needs varies significantly across these funding models.

Fully insured plans offer convenience but limited flexibility. Think of them as pre-packaged meals—they’re ready to go, but you can’t easily remove ingredients you don’t want or add ones you do. These plans must include all state-mandated benefits, and you have minimal control over plan design. If your workforce has unique needs, this one-size-fits-all approach might leave many employees unsatisfied.

Self-insured plans offer maximum flexibility—they’re the made-from-scratch meal of health plans. You can tailor benefits to your workforce’s specific needs, exclude state-mandated benefits that don’t make sense for your team (though federal requirements still apply), and access detailed claims data to make informed decisions about future plan adjustments. This level of customization can be a powerful tool for attracting and retaining talent.

Level-funded plans strike a balance, offering more customization than fully insured plans while being easier to implement than fully self-insured options. Many carriers allow you to design plans that reflect your employees’ needs, often including innovative benefits like telemedicine, expanded mental health services, and wellness programs. You’ll also gain access to claims data, helping you make smarter decisions about your benefits strategy.

A human resources manager at a growing company explained the impact of this flexibility: “When we switched to a level-funded plan, we added coverage for alternative therapies our younger workforce values, while maintaining strong coverage for traditional medical needs. This flexibility has been a powerful recruitment tool, helping us compete for talent against much larger companies.”

Understanding these key differences between fully insured vs self-insured vs level-funded plans provides the foundation you need to make an informed choice for your business. Each approach has its strengths and challenges, and the right option depends on your company’s specific circumstances, risk tolerance, and goals.

Pros and Cons of Each Plan Type

Choosing between fully insured vs self-insured vs level-funded health plans isn’t a one-size-fits-all decision. Each approach comes with its own set of advantages and trade-offs that could make it either perfect or problematic for your business. Let’s break down what you can expect from each option.

Pros and Cons of Fully Insured Plans

The fully insured approach is like buying an all-inclusive vacation package – you know exactly what you’re paying upfront, with no surprise bills waiting for you later.

Predictable costs make fully insured plans the comfort food of health insurance. You’ll pay the same premium each month, making budgeting straightforward and reliable. For smaller businesses or those with tight cash flow constraints, this predictability can be invaluable.

The minimal financial risk is another significant advantage. Your insurance carrier shoulders the burden if an employee needs expensive care. As one small business owner told us, “When my employee needed a $300,000 cancer treatment, I was grateful we weren’t self-funded. That would have devastated our finances.”

You’ll also enjoy administrative simplicity with a fully insured plan. The carrier handles claims processing, member services, and most of the paperwork. This means your HR team can focus on other priorities instead of becoming health insurance experts.

On the flip side, fully insured plans typically come with higher overall costs. You’re paying for the carrier’s profit margin, administrative fees, and risk charges – essentially paying a premium for that peace of mind. These plans also offer limited control over plan design. Want to cover acupuncture but not chiropractic care? Too bad – you’ll generally have to accept the carrier’s pre-packaged benefits.

Perhaps most frustratingly, there’s no potential for savings if your employees stay healthy. Even if your team files minimal claims, that money stays with the insurance company. And when renewal time comes around, you might face significant premium increases based on your prior year’s claims or overall market trends.

Pros and Cons of Self-Insured Plans

Self-insured plans are like buying the ingredients and cooking your own meal instead of ordering takeout – potentially cheaper and customized exactly to your taste, but requiring more work and skill.

The cost savings potential is the biggest draw here. By eliminating carrier profit margins and risk charges, many employers save 10-15% on healthcare costs. These savings compound over time and can be substantial for larger organizations.

You’ll also gain complete plan design control. Want to add coverage for fertility treatments while reducing copays for preventive care? You can tailor benefits to your workforce’s specific needs rather than accepting a one-size-fits-all approach.

Data transparency is another powerful advantage. You’ll receive detailed claims data (appropriately anonymized for privacy), allowing you to spot trends, identify cost drivers, and make informed decisions about your benefits strategy.

Self-funded plans also offer regulatory advantages, including exemption from state premium taxes and some state-mandated benefits, though you’ll still need to comply with federal regulations.

The most significant drawback is the financial risk involved. Without proper stop-loss insurance, a few catastrophic claims could seriously damage your company’s finances. This approach also brings cash flow variability – some months might see minimal claims while others could bring substantial expenses.

The administrative burden increases substantially too. You’ll typically need to hire a Third-Party Administrator (TPA) to process claims and handle day-to-day operations. As one HR director put it, “Self-funding isn’t just a financial decision – it’s also an operational one. Make sure you have the infrastructure to support it.”

Pros and Cons of Level-Funded Plans

Level-funded plans represent the middle ground – like a meal kit delivery service that gives you fresh ingredients and a recipe but saves you from shopping and meal planning.

These plans offer predictable costs with savings potential – you make fixed monthly payments (helping with budgeting) while maintaining the possibility of year-end refunds if claims are lower than projected. For many small to mid-sized businesses, this combines the best aspects of both fully insured and self-funded approaches.

The reduced financial risk compared to traditional self-funding makes level-funding particularly attractive. Built-in stop-loss coverage protects against catastrophic claims, creating a safety net that many smaller employers find reassuring.

You’ll also enjoy greater plan flexibility than fully insured options. While not offering the complete freedom of self-funding, level-funded plans typically allow more customization to meet your employees’ specific needs.

Like self-funded plans, level-funded arrangements provide data access to help you understand utilization patterns and make informed decisions about your benefits strategy.

However, level-funding isn’t perfect. Those potential refunds aren’t guaranteed – they only materialize if your claims experience is favorable. You might also face higher administrative costs than with fully insured plans, as you’re essentially paying for both insurance and administrative services.

The renewal considerations can be complex too. If your claims are higher than expected, you might face significant rate increases at renewal – sometimes even higher than you’d see with a fully insured plan.

“We switched to level-funding three years ago,” shared the owner of a 40-employee marketing agency. “The first year, we got a $15,000 refund. The second year, our claims were high, so no refund. But overall, we’re still paying less than we would with a fully insured plan, and I sleep better knowing we have predictable monthly payments.”

For many small to mid-sized businesses, level-funding hits the sweet spot between financial protection and potential savings. That’s why these plans have seen explosive growth, with adoption among small firms jumping from 7% in 2019 to 34% in 2023.

The right choice between fully insured vs self-insured vs level-funded ultimately depends on your organization’s size, risk tolerance, financial stability, and benefits philosophy. Many businesses find their approach evolves as they grow, often starting with fully insured plans and gradually moving toward level-funded or self-funded arrangements as they gain size and stability.

How to Decide Which Plan Is Right for Your Business

Choosing between fully insured vs self-insured vs level-funded health plans isn’t a one-size-fits-all decision. Your company’s unique characteristics will guide you toward the option that offers the best balance of cost, risk, and benefits for your situation. Let’s explore the key factors you should consider before making this important choice.

Assessing Your Company’s Size and Financial Stability

When it comes to health plan funding, size really does matter. Your employee count often serves as the first signpost pointing toward your ideal funding model.

If you’re running a small business with fewer than 50 employees, you’ve probably been steered toward fully insured plans in the past. The conventional wisdom was that smaller companies couldn’t handle the risk of alternative funding models. But times are changing! We’re seeing a dramatic shift, with 42% of small firms embracing level-funded plans in 2025 – a remarkable increase from just 7% in 2019. These businesses are finding that level-funding offers a sweet spot of predictability with the potential for year-end savings.

For mid-sized companies with 50-200 employees, level-funded arrangements often hit the bullseye. You have enough employees to create somewhat predictable claims patterns, but perhaps not enough to fully self-fund without some anxiety. As one of our clients with 75 employees told us, “Level-funding gives us budget certainty month-to-month, but we’ve still gotten refunds three years running. It’s the perfect middle ground for us.”

Large organizations with over 200 employees predominantly choose self-funding – about 85% of them, according to 2025 data. With a larger employee pool, your claims become more predictable, allowing you to better absorb monthly fluctuations while capturing significant savings by cutting out the middleman’s profit margin.

Your financial stability matters just as much as your headcount. Before jumping into self-funding or even level-funding, take an honest look at your company’s financial picture:

Cash flow consistency is crucial for self-funded plans. Can your business handle a month where claims might be double the average? If your revenue fluctuates seasonally or you’re operating with tight margins, a fully insured or level-funded approach might help you sleep better at night.

Your risk tolerance plays a major role too. Some business owners are comfortable with uncertainty if it means potential savings, while others prefer the peace of mind that comes with predictable costs. As one financial advisor put it, “The question isn’t just whether you can afford self-funding, but whether you can afford the stress of not knowing exactly what next month’s healthcare bill will be.”

For self-funded and level-funded plans, you’ll need to consider establishing reserves to cover unexpected claims. Having this financial cushion is essential for weathering the inevitable ups and downs of healthcare costs.

Evaluating Employee Needs and Preferences

Your employees aren’t just entries on a spreadsheet – they’re real people with unique healthcare needs and preferences. Understanding these needs is essential to choosing the right funding model.

Start by analyzing your workforce demographics. A younger employee population typically generates fewer claims, making self-funded or level-funded plans more financially attractive. If your team includes many older employees or those with chronic conditions, you might benefit from the predictability of a fully insured plan – or you might find that the customization possible with alternative funding allows you to better support their specific health needs.

Take time to examine past healthcare utilization patterns. If you’ve been fully insured, request claims data from your carrier (they may provide summaries without revealing individual information). This data can reveal trends that help you project future costs and identify areas where customized benefits might make sense.

Don’t forget to actually ask your employees what they value most. Simple surveys can uncover surprising insights about which benefits matter most to your team. One HR director told us, “We found our employees cared more about access to mental health services than lower deductibles. Our level-funded plan let us shift resources to better mental health coverage, which would have been difficult with our old fully insured plan.”

Health benefits play a huge role in recruitment and retention. Industry surveys consistently show that over 90% of employees rate health benefits as important in their job decisions. The right health plan isn’t just a cost center – it’s a powerful tool for building and maintaining your workforce.

Understanding Regulatory Compliance Requirements

Each funding approach comes with its own regulatory landscape. Understanding these differences helps you avoid compliance headaches down the road.

With fully insured plans, the insurance carrier handles most compliance requirements. They ensure the plan meets state insurance regulations and includes all mandated benefits. Your administrative burden is relatively light, with simpler ACA reporting requirements. This simplicity is one reason many small businesses have traditionally chosen fully insured plans.

Self-insured plans shift more compliance responsibilities to your shoulders. These plans are primarily regulated by federal law (ERISA) rather than state insurance regulations. While this exempts you from state premium taxes and mandated benefits, it also means you’re responsible for additional compliance tasks like PCORI fee filings, more complex ACA reporting (Forms 1094-C and 1095-C), nondiscrimination testing, and determining COBRA premiums.

Level-funded plans generally carry similar compliance requirements to self-funded plans, though many TPAs provide administrative support to help you steer these obligations. As one benefits compliance expert noted, “Don’t assume your TPA will handle everything. Get clarity on exactly who’s responsible for each compliance task before implementing a new funding model.”

The right choice between fully insured vs self-insured vs level-funded plans depends on finding the sweet spot where your company size, financial stability, employee needs, and appetite for administrative responsibilities all align. At NPA Benefits, we’ve guided countless businesses through this decision process, helping them find the funding model that offers the best value while supporting their unique workforce.

Frequently Asked Questions about Fully Insured, Self-Insured, and Level-Funded Plans

What is the main difference between fully insured and self-insured plans?

When comparing fully insured vs self-insured plans, it all comes down to who’s holding the financial risk bag.

With a fully insured plan, your insurance carrier takes on all the risk. Your company pays those predictable monthly premiums, and the carrier handles everything else—regardless of how many claims your employees file or how expensive they are. It’s like paying for an all-you-can-eat buffet: you pay the same price whether your employees take one plate or five.

“I sleep better at night knowing exactly what our healthcare costs will be each month,” shared one small business owner. “For us, the predictability outweighs the potential savings of other options.”

In contrast, with a self-insured plan, your company steps into the insurer’s shoes. Instead of paying premiums, you’re directly responsible for your employees’ healthcare claims as they happen. This approach can save you money (often 10-15%) by eliminating the insurance company’s profit margin and risk charges, but it introduces more financial uncertainty.

As one CFO put it, “Self-funding is like cooking at home instead of eating out. You’ll probably save money overall, but you need to be prepared for the occasional grocery bill that’s higher than expected.”

Are level-funded plans suitable for small businesses?

Absolutely! Level-funded plans have become increasingly popular among small businesses for good reason. They offer a “best of both worlds” approach that many small companies find appealing.

The numbers tell the story: back in 2019, only about 7% of small firms (3-199 employees) offered level-funded plans. By 2025, that number has jumped to 42%—a dramatic increase in just six years.

Why are small businesses flocking to level-funding? These plans provide the monthly payment predictability of fully insured plans while still offering the potential for savings if your employees have fewer claims than expected. The built-in stop-loss coverage protects you from those financial nightmares that keep small business owners up at night.

“We switched to level-funding three years ago,” shared the owner of a local accounting firm with 28 employees. “We’ve received refunds each year—last year it was over $22,000. That’s money we’ve been able to reinvest in better office equipment and employee bonuses.”

Level-funded plans work particularly well for small businesses with relatively healthy employees. If your workforce is young or generally healthy, you might be overpaying with a traditional fully insured plan that pools your risk with other, potentially less healthy groups.

Of course, level-funding isn’t perfect for everyone. You’ll need stable cash flow and comfort with some additional administrative responsibilities. But for many small businesses looking to balance predictability with savings potential, level-funded plans hit a sweet spot in the fully insured vs self-insured vs level-funded spectrum.

How does stop-loss insurance protect employers?

Stop-loss insurance is the unsung hero of self-funded and level-funded health plans. Without it, few employers would dare to venture beyond fully insured options.

Think of stop-loss insurance as your financial safety net. It protects you from those rare but potentially devastating healthcare claims that could otherwise wreak havoc on your company’s finances.

There are two main types of stop-loss coverage, and they work together to create a comprehensive protection system:

Individual (Specific) Stop-Loss limits your liability for any single claim. Let’s say you have a $50,000 specific threshold. If an employee needs a complex surgery costing $300,000, you’re only responsible for the first $50,000—the stop-loss insurance picks up the remaining $250,000. This protects you from those rare but financially devastating health events.

Aggregate Stop-Loss caps your total annual claims exposure. If your company’s overall claims exceed a predetermined threshold (typically 125% of expected claims), the stop-loss insurance covers the excess. This protects against the scenario where you have lots of medium-sized claims that collectively exceed your budget.

A human resources director shared this revealing experience: “Last year, one of our employees was diagnosed with a rare form of cancer. The treatment cost over $600,000. Thanks to our stop-loss insurance, our financial exposure was limited to $75,000. Without that protection, we might have had to make some very difficult decisions about our benefits program—or worse.”

In level-funded arrangements, stop-loss coverage is already built into your monthly payment, creating a seamless safety net. For self-funded plans, you’ll purchase this coverage separately, allowing you to customize the thresholds based on your risk tolerance and financial resources.

As one benefits consultant puts it: “Stop-loss insurance is what makes self-funding and level-funding accessible to companies of all sizes. It transforms an potentially unlimited financial liability into a manageable, budgetable expense.”

Conclusion

Navigating the landscape of fully insured vs self-insured vs level-funded health plans isn’t simple, but making an informed choice can significantly impact both your bottom line and employee satisfaction. The truth is, there’s no perfect solution that works for every organization – the right approach depends on your unique situation, goals, and comfort with financial risk.

Healthcare costs aren’t slowing down anytime soon (with a projected 7% increase coming in 2025), making it increasingly worthwhile to look beyond traditional fully insured arrangements. Self-funded and level-funded options can offer meaningful savings and flexibility, but they require honest assessment of your company’s financial stability, size, and administrative capabilities.

When we work with clients at NPA Benefits, we often find that each funding model shines in different scenarios:

Fully insured plans typically work best for smaller businesses that value predictability above all else. If you prefer knowing exactly what you’ll pay each month and want to minimize administrative hassle, this traditional approach might be your best fit – even if it means paying a premium for that peace of mind.

Self-insured plans generally serve larger organizations well, particularly those with healthy cash reserves and a relatively stable workforce health profile. If you have sophisticated financial management capabilities and are comfortable with some month-to-month variability in exchange for potential savings, self-funding could be your path to significant cost reduction.

Level-funded plans have become the “goldilocks” option for many small to mid-sized businesses. They offer a compelling middle ground – the predictable monthly payments you need for budgeting, built-in protection against catastrophic claims, and the potential for year-end refunds when claims run lower than expected.

At NPA Benefits, we’ve spent years helping employers untangle these complex decisions. We understand that choosing a health plan funding strategy isn’t just a financial calculation – it’s a critical part of your overall employee benefits package that directly impacts your ability to attract and retain talent. When 92% of employees rate health benefits as important in job satisfaction surveys, getting this decision right matters more than ever.

Your employees don’t just want health coverage; they want quality, accessible care that meets their unique needs. The funding model you choose directly affects how flexible and customized your plan can be. While fully insured plans offer limited customization, self-funded and level-funded arrangements give you more freedom to design benefits that truly resonate with your workforce.

Ready to explore whether self-funded or level-funded plans might be right for your organization? We’ve created detailed resources comparing level funding vs self-funding and explaining the differences between self-funded vs level-funded approaches.

We’re here to help you steer the complexities of health insurance funding and create a solution custom to your specific needs. The right funding strategy can help you control costs without sacrificing the quality benefits your employees deserve. Reach out today, and let’s start the conversation about optimizing your employee benefits approach.